|

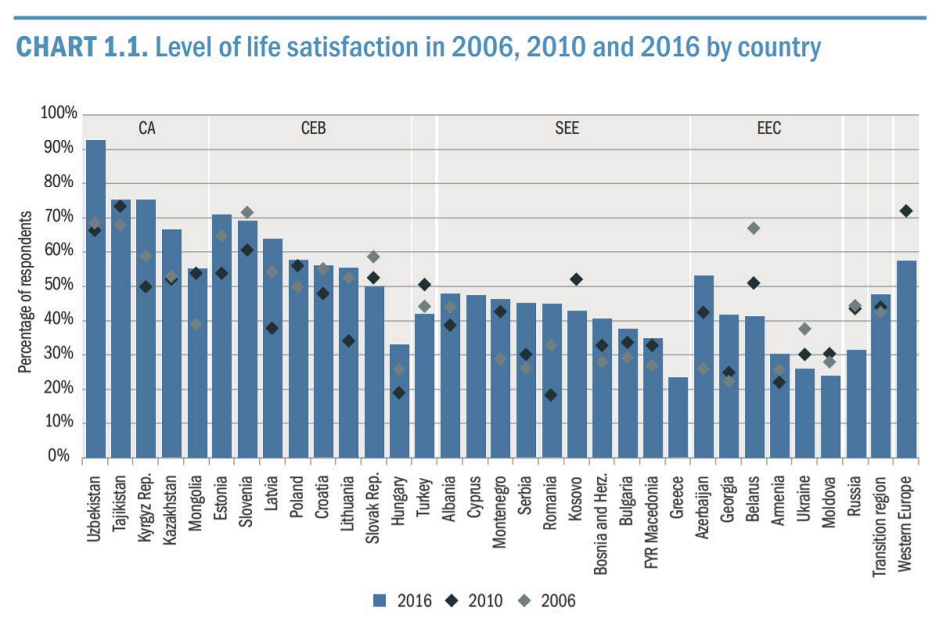

Central Eurasia: Making Markets Another look at the map

Source: World Bank, World Development Indicators

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

1989 |

1995 |

2000 |

2005 |

2010 |

|

|

Albania |

5 |

60 |

75 |

75 |

75 |

|

Armenia |

10 |

45 |

60 |

75 |

75 |

|

Azerbaijan |

10 |

25 |

45 |

60 |

75 |

|

Belarus |

5 |

15 |

20 |

25 |

30 |

|

Bosnia/Hrz |

na |

na |

35 |

55 |

60 |

|

Bulgaria |

10 |

50 |

70 |

75 |

75 |

|

Croatia |

15 |

40 |

60 |

65 |

70 |

|

Czech Rep. |

5 |

70 |

80 |

80 |

80 |

|

Estonia |

10 |

65 |

75 |

80 |

80 |

|

Macedonia |

15 |

40 |

55 |

65 |

70 |

|

Georgia |

10 |

30 |

60 |

65 |

75 |

|

Hungary |

5 |

60 |

80 |

80 |

80 |

|

Kazakhstan |

5 |

25 |

60 |

65 |

65 |

|

Kirgiz Rep. |

5 |

40 |

60 |

75 |

75 |

|

Latvia |

10 |

55 |

65 |

70 |

70 |

|

Lithuania |

10 |

65 |

70 |

75 |

75 |

|

Moldova |

10 |

30 |

50 |

60 |

65 |

|

Mongolia |

0 |

40 |

60 |

70 |

75 |

|

Montenegro |

na |

na |

na |

na |

65 |

|

Poland |

30 |

60 |

70 |

75 |

75 |

|

Romania |

15 |

45 |

60 |

70 |

70 |

|

Russia |

5 |

55 |

70 |

65 |

65 |

|

Serbia |

na |

na |

na |

na |

60 |

|

Slovakia |

5 |

60 |

80 |

80 |

80 |

|

Slovenia |

10 |

50 |

65 |

65 |

70 |

|

Tajikistan |

10 |

25 |

40 |

55 |

55 |

|

Turkmenistan |

10 |

15 |

25 |

25 |

25 |

|

Ukraine |

10 |

45 |

60 |

65 |

60 |

|

Uzbekistan |

10 |

30 |

45 |

45 |

45 |

EBRD Assessment of Transition Quality (AQP) Indicators

see explanations of terms here

|

Competitive |

Well-governed |

Green |

Inclusive |

Resilient |

Integrated |

|

|

|

2019 |

2019 |

2019 |

2019 |

2019 |

2019 |

|

Estonia |

7.63 |

8.27 |

6.42 |

7.66 |

8.11 |

7.49 |

|

Slovenia |

7.09 |

6.65 |

7.08 |

7.35 |

7.73 |

7.14 |

|

Poland |

6.76 |

6.82 |

6.52 |

6.81 |

7.86 |

6.81 |

|

Slovak Republic |

6.76 |

6.21 |

6.87 |

6.54 |

7.97 |

7.10 |

|

Cyprus |

6.68 |

7.07 |

6.32 |

6.66 |

5.60 |

7.68 |

|

Latvia |

6.48 |

6.66 |

6.77 |

7.07 |

7.89 |

7.00 |

|

Hungary |

6.36 |

6.01 |

6.27 |

6.65 |

7.15 |

6.84 |

|

Lithuania |

6.27 |

6.85 |

6.63 |

6.94 |

7.34 |

7.05 |

|

North Macedonia |

6.02 |

5.57 |

5.16 |

5.90 |

5.93 |

5.75 |

|

Romania |

6.01 |

6.04 |

6.14 |

5.74 |

7.11 |

6.75 |

|

Russia |

5.83 |

5.90 |

5.09 |

6.83 |

6.42 |

5.00 |

|

Greece |

5.78 |

5.22 |

6.13 |

6.24 |

7.04 |

6.41 |

|

Bulgaria |

5.71 |

5.79 |

6.04 |

6.24 |

6.91 |

6.85 |

|

Croatia |

5.64 |

5.97 |

6.38 |

6.39 |

7.47 |

6.54 |

|

Montenegro |

5.44 |

6.11 |

5.41 |

5.98 |

6.44 |

6.15 |

|

Serbia |

5.36 |

5.52 |

5.79 |

6.16 |

5.86 |

5.99 |

|

Kazakhstan |

5.26 |

5.67 |

5.36 |

6.46 |

5.95 |

4.91 |

|

Belarus |

5.17 |

5.15 |

6.22 |

6.63 |

4.16 |

5.43 |

|

Albania |

5.14 |

5.11 |

4.49 |

5.31 |

5.22 |

5.66 |

|

Georgia |

4.98 |

6.40 |

5.32 |

5.14 |

6.19 |

6.35 |

|

Armenia |

4.97 |

5.78 |

5.72 |

5.97 |

6.40 |

5.45 |

|

Kosovo |

4.78 |

4.56 |

3.47 |

5.28 |

5.18 |

4.67 |

|

Ukraine |

4.77 |

4.78 |

5.87 |

6.21 |

5.67 |

4.75 |

|

Bosnia/Herzegovina |

4.68 |

4.53 |

5.20 |

5.48 |

5.91 |

5.08 |

|

Azerbaijan |

4.39 |

5.79 |

5.35 |

4.94 |

3.97 |

5.59 |

|

Moldova |

4.36 |

4.81 |

4.68 |

5.58 |

5.82 |

4.94 |

|

Mongolia |

4.22 |

5.11 |

5.36 |

5.19 |

5.37 |

4.53 |

|

Kyrgyz Republic |

4.04 |

4.12 |

4.48 |

4.62 |

5.12 |

4.92 |

|

Uzbekistan |

3.39 |

4.45 |

4.41 |

5.41 |

3.96 |

3.93 |

|

Tajikistan |

3.25 |

3.63 |

4.84 |

5.05 |

3.68 |

3.51 |

|

Turkmenistan |

2.81 |

2.28 |

4.09 |

5.41 |

3.21 |

3.97 |

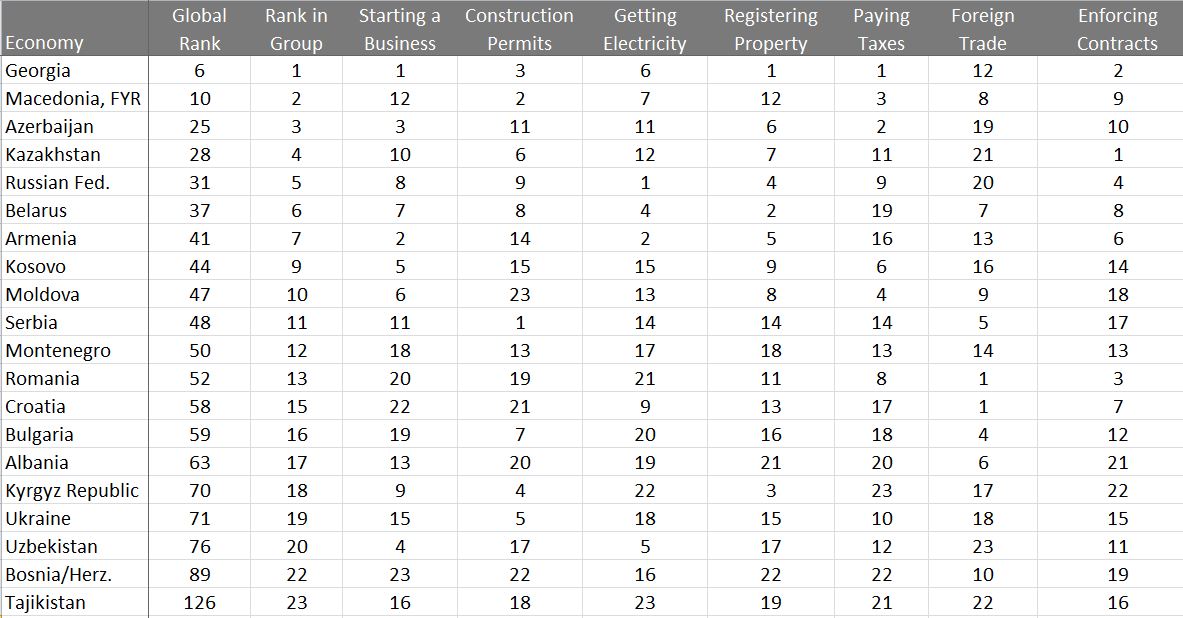

Ease of Doing Business Rankings, 2019

{kind=link}

The World Bank, doingbusiness.org